Thought pieceUnlocking Profitability Through Transaction-Led Digital Banking

Fuelling customer growth through strategic transformation and smarter segmentation

By Nick Drewett, Chief Commercial Officer, Engine by Starling and Ravi Kittane, Partner, Financial Services Technology Consulting, EY Malaysia

Customer expectations are evolving and banking is no longer viewed as a standalone utility, but as a primary enabler of lifestyle and business goals. In today’s landscape, strong customer service and seamless digital experiences have become a critical driver of customer acquisition and deposit growth. Digital engagement is now a leading indicator of account primacy, as digital-first players show how simple onboarding, intuitive journeys and real-time decisioning can translate into trust, loyalty and low-cost deposits. The transaction-led model reinforces this shift, where value is created at the moment of need rather than through traditional product pushes. A recent example from India1 illustrates this well: a food delivery app offers customers small, short-term loans at the end of the month, using consumption data to manage risk and embed finance into everyday activity.

For banks, this highlights the opportunity to use embedded finance and data-driven journeys to meet real-time customer needs while building a more efficient, sustainable deposit franchise.

Britain’s first digital bank, Starling, serves as a compelling example of the transaction-led model. By addressing specific friction points for small and medium enterprises (SMEs), Starling captured a 9.4% share of the UK SME market and achieved profitability with a conservative loan-to-deposit ratio (LDR) of about 40%. They have also recently launched the UK’s first agentic AI financial assistant, helping customers manage day-to-day finances. Crucially, they achieved this while maintaining strict operational discipline, operating with a cost-to-serve of just £42.40 per active customer while still offering 24/7 human support.

This strategy of segment-led focus and operational efficiency is not unique to the UK; it is being validated globally. In Vietnam, Cake by VPBank successfully replicated this approach by targeting Gen Z and millennials, a segment often overlooked by traditional players. Rather than competing on general utility, Cake differentiated itself through “brilliant basics” and embedded small-ticket finance, offering micro-lending solutions where drivers can apply for loans with a few clicks and receive instant decisions. According to a 2024 report in The Digital Banker2 , Cake acquired five million users and reached profitability in 2024, just three-and-a-half years after launch. supported by an AI-driven technology model that enables two-minute onboarding and processes 400,000 credit applications a month

Both Starling and Cake demonstrate that high-touch service and low-cost operations can coexist but are most effectively achieved when technology is used to decouple operational costs from customer growth.

Most banks were built for a lending-first world where customers borrowed episodically and most movement of money could be settled at day’s end. Cash and branches did a lot of the work to fulfil the day-to-day banking needs of consumers. Personal service once came from staff who knew you by name.

Today, everyday banking is digital and in real time; agents meet people they’ve never seen and still need a full, instant view. In a digital, deposit-driven model, payments and service interactions happen constantly; the bar is a high-fidelity platform that can process at scale with accuracy and resilience.

Despite banks globally investing heavily in digitalisation, many struggle to replicate the efficiency and agility of leaders. The challenge is not a lack of ambition but overcoming deep structural inhibitors across three key dimensions.

Genuine agility and efficiency are almost impossible to achieve without driving systems modernisation right to the core. The architecture of legacy systems simply gets in the way of innovation, customer centricity and demands an expensive operating model to maintain. At the same time, its dependence on multiple third‑party vendors diluted accountability and slowed delivery cycles — ultimately raising the cost of iterating and improving new propositions over time.

There are three obstacles to modernisation:

1. Rigid product structures: Most incumbents remain locked in product-centric structures. They focus on pushing standard banking products rather than addressing specific customer friction points. This rigid approach restricts agility. It makes it difficult to pivot quickly toward emerging market needs. Consequently, banks often find themselves reacting to competitors rather than innovating new solutions. They miss the demand for the real-time services that drive primary account status.

2. Operational silos: Execution is further constrained by fragmented operating practices across the bank. Teams working in isolation create friction that prevents end-to-end ownership of the customer experience. Innovation is further stifled by rigid waterfall delivery models. Business cases often take months to approve, so features risk becoming obsolete by the time they reach the customer.

3. Aging technology stack: Operational constraints in many banks are intensified by the underlying technology. Reliance on monolithic infrastructure drives up integration and enhancement costs, making it difficult to serve niche segments profitably. Critical data remains locked within legacy systems, limiting bank‑wide personalisation and reducing visibility for front‑line teams.

What banks should consider:

To solve these structural problems, banks should look to more than just launching a new app or upgrading a single system. Success is supported by a holistic approach, where the business model, operations and technology all work together.

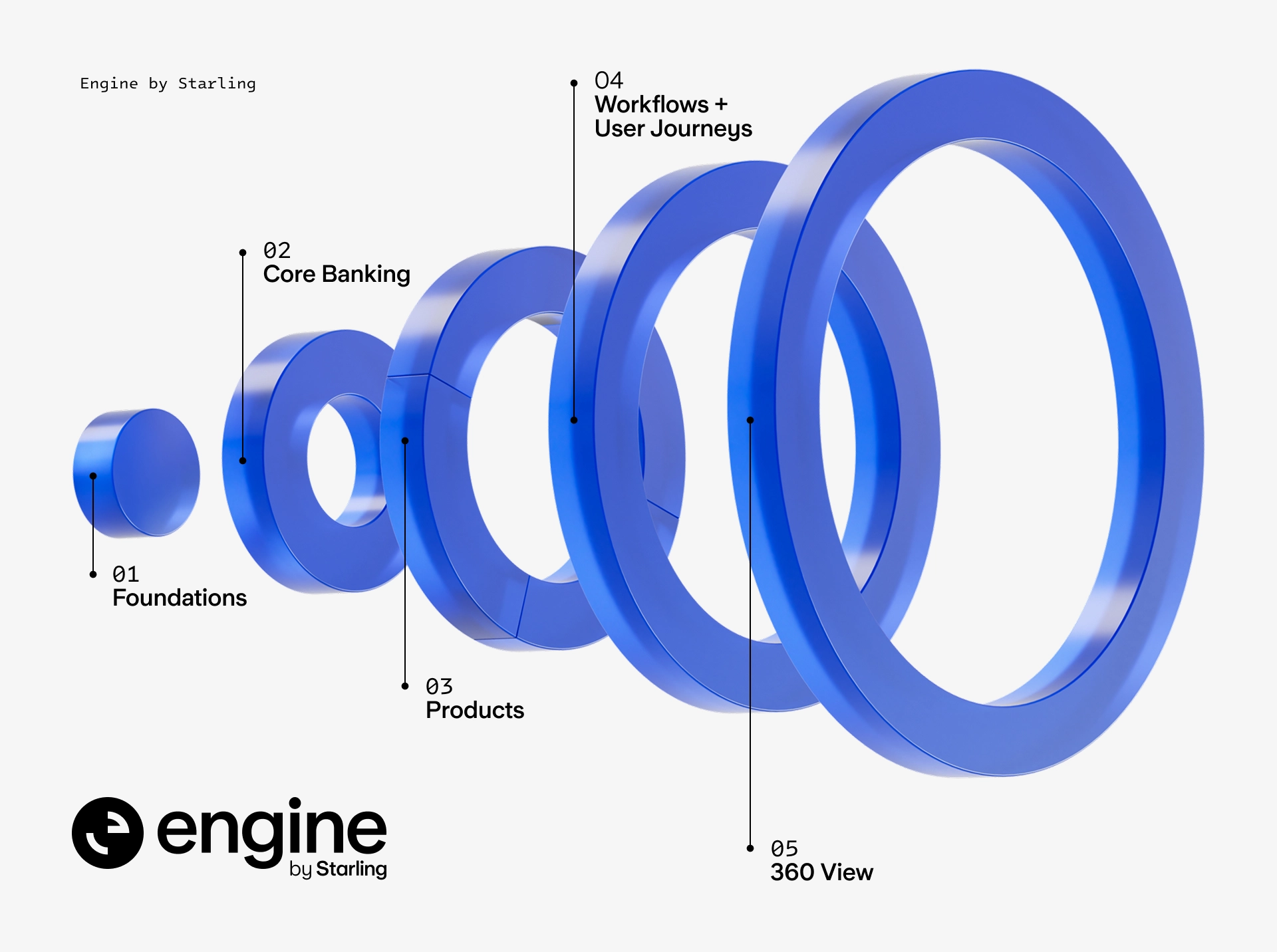

This integration is exemplified by Engine by Starling, a cloud-native, managed service banking platform that encapsulates the technology and processes required to run a modern digital bank. By adopting such a platform, banks can simultaneously address challenges across their business model, operating model and technology stack.

A three-pronged execution strategy of prioritising high-value customer segments, unifying cross-functional teams through shared technology, and establishing a real-time, cloud-native architectural foundation, enables banks to move from a generic offering to a niche over performer.

Focusing on segments to increase market share

Success is well supported by a 360° approach where the institution is structured around deep segment knowledge rather than isolated product verticals. Winning banks identify high-value targets and build value propositions around solving specific customer or employee friction points, shifting their focus from generic product sales to holistic customer centricity.

Instead of attempting to be a generalist utility, Starling Bank identified a crossover between retail and SME, an underserved segment of sole proprietors and small businesses, and built a targeted proposition around them. They moved beyond basic payments to solve the real day-to-day demands of business owners, embedding tools like a “Tax Toolkit” and seamless accounting integration directly into the app. This fundamental choice to prioritize customer utility naturally drove account primacy and a 9.4% market share.

This segment-led focus is validated globally across different demographics. OakNorth targeted the “missing middle” with data-driven lending for medium-sized enterprises3, while Judo Bank achieved profitability in just two-and-a-half years by building a relationship-led model specifically for the SME lending sector4.

Similarly, Superbank Indonesia champions an ecosystem-led approach by integrating directly into the Grab, Singtel and Emtek network; with embedded products such as “OVO Nabung” and “Pinjaman Atur Sendiri”, they have been able to underwrite the underbanked gig economy and micro-SMEs, scaling to five million users and achieving profitability within 12 months5.

Salt Bank in Romania and AMP Bank in Australia both used Engine’s configurable platform to go to market with a rich digital offering in just 12 months. According to a 2025 report by Fin Extra6, Salt Bank attracted more than 500,000 customers within its first year (about 4% Romania’s adult population) and has gone on to win awards including “Best Digital Bank” and “Best Use of Tech in Retail Banking”.

Their success and interactive, monthly rollout of new products and features demonstrate an innovation velocity that allows banks to test segment specific propositions without being held back by multi-year development cycles.

Enabling teams and technology to move as one

Delivering a new business model is most effective with a corresponding shift in how teams operate. Crucially, operational efficiency is empowered by technology that unifies the bank.

Cross-functional teams are supported by a single pane of glass, evidenced by Engine’s “Management Portal” that mirrors the customer’s mobile app experience for the support agent. Because the front-line staff see exactly what the customer sees in real time, they can resolve complex queries instantly without “swivel-chairing” between disjointed systems.

This seamless synchronisation between the front-end app and the back-office agent portal creates the agency required for staff to own the customer experience, as proven by Starling Bank's very high first call resolution rate.

Empowering the front-line is made more effective when the organisation behind them is equally agile. There is a growing strategic need for banks to shift from viewing IT as a back-office support function to becoming an “engineering-led” organisation. This means engineers are present at every level of decision-making and are expected to be domain experts who own their product roadmaps, rather than just executing tickets handed down by business owners. This is supported by a deliberately flat organisational structure, typically no more than three levels from a junior engineer to the chief technology officer, which minimises the “distance to decision” and prevents the formation of silos.

True agility is often derived less from adopting rigid methodologies and more from optimising for change through automation and autonomy. Starling uses a “continuous delivery” model, running more than 200,000 automated tests in 30 minutes so that software is always production-ready. The resilience of cloud-native architecture is what enables them to operate at this level of efficiency.

This approach allows the bank to release small, iterative updates based on real-time feedback rather than risking “big bang” launches after months of development. While this originated in tech companies and challenger banks, it is replicable for incumbents; a global financial institution has seen success adopting similar cross-functional “tribes” to pilot this way of working, improving their net promoter score (NPS) by 60 points and employee engagement by 88%.

Designing technology architecture for real-time customer-centric banking

The difference between cloud native Gen 4 systems, and earlier solutions, is much deeper than the question of where the application is hosted: a bank’s data centre or public cloud. The architecture of Gen 4 is what enables customer centricity. Customers expect a bank to be on their side, helping them to manage their finances in new and innovative ways, regularly launching new capabilities at a pace that older systems cannot match. Customers expect their bank to be available 24/7: outages are simply unacceptable and data must be updated in real time.

A bank may be constrained when running on a third generation (Gen 3) legacy core, where data is processed in overnight batches and trapped in monolithic silos. In a Gen 3 environment, a customer might have a loan approved at 9:00 a.m., but the bank’s systems and its support agents won’t see the final settlement until the next day. To match the speed of the modern customer, banks should consider a fourth generation (Gen 4) architecture that is cloud-native, led by application programming interface (API) and fundamentally real time.

The structural difference lies in the architecture. Unlike rigid legacy systems where a small change triggers months of regression testing, Gen 4 platforms utilise microservices. This breaks the bank down into small, independent building blocks, separate components for “payments”, “cards” and “onboarding”.

This modularity minimises integration complexity and enables the bank to update specific features, whilst mitigating the risk of system-wide disruptions. It enables the “continuous delivery” model where software updates are deployed securely and reliably multiple times a day, allowing the bank to adapt to market changes instantly rather than waiting for quarterly release cycles.

The new era of banking is defined by the core of the customer relationship: the effortless execution of everyday transactions. As banking integrates deeper into the daily lives of consumers and businesses, the underlying business model must shift to prioritise this constant engagement. However, this needs to go beyond surface-level changes; it requires a fundamental core transformation powered by Gen 4 cloud-native systems.

In today’s market, changing customer behaviours have reset the bar for excellence. A high-quality mobile app will no longer shift the dial on customer loyalty. To effectively acquire and retain customers, banks must deliver innovation and customer centricity that an aging infrastructure simply cannot support.

While core modernisation is a significant strategic undertaking, it is a worthwhile endeavour. By rebuilding on a cloud-native foundation, banks move beyond the limitations of legacy systems to unlock a modern business model characterised by high NPS, customer growth and a lower cost-to-serve. Ultimately, this transformation enables banks to secure the most valuable asset in the digital age: account primacy and the low-cost deposit growth that comes with it.

- Five questions about banking in today’s digital age, answered, EYGM Limited, 2021 (https://www.ey.com/en_gl/insights/banking-capital-markets/five-questions-about-banking-in-todays-digital-age-answered)

- Cake Digital Bank Achieves Profitability in 3.5 Years, Poised to Join The Top 5% of Profitable Digital Banks Worldwide, The Digital Banker, 2024 (https://thedigitalbanker.com/cake-digital-bank-achieves-profitability-in-3-5-years-poised-to-join-the-top-5-of-profitable-digital-banks-worldwide/)

- How our entrepreneurial approach is transforming business solutions, Oaknorth, 2024 (https://oaknorth.co.uk/blog/how-our-entrepreneurial-approach-is-transforming-business-solutions/)

- Opportunities aplenty for digital banks but no threat to incumbent banks — yet, The Edge, 2025 (https://theedgemalaysia.com/node/782623)

- Superbank posts $4.9m Q3 profit, Tech In Asia, 2025 (https://www.techinasia.com/news/superbank-posts-4-9m-q3-profit)

- Salt Bank reaches 500,000 customer one year on from launch with Starling Engine, Fin Extra, 2025 (https://www.finextra.com/pressarticle/105185/salt-bank-reaches-500000-customer-one-year-on-from-launch-with-starling-engine)

Chief Commercial Officer,

Engine by Starling

Partner, Financial Services Technology Consulting,

EY Malaysia

The views reflected in this article are the views of the author and do not necessarily reflect the views of the global EY organisation or its member firms. EY Malaysia refers to Ernst & Young Consulting Sdn. Bhd.