Spotlight

Driving digital banking innovation in North America

By Natalie Jack and Olivia Stephenson

Here at Engine by Starling, we’re supporting banks around the world on their digital transformation journeys, and recently our plans for North America came into focus.

The US market, in particular, presents a significant opportunity given the thousands of mid-tier banks and credit unions in need of better digital servicing. By leveraging Starling Bank’s specialist knowledge and best-in-class proprietary technology, Engine enables these organisations to redefine the customer experience, from the core to the frontend.

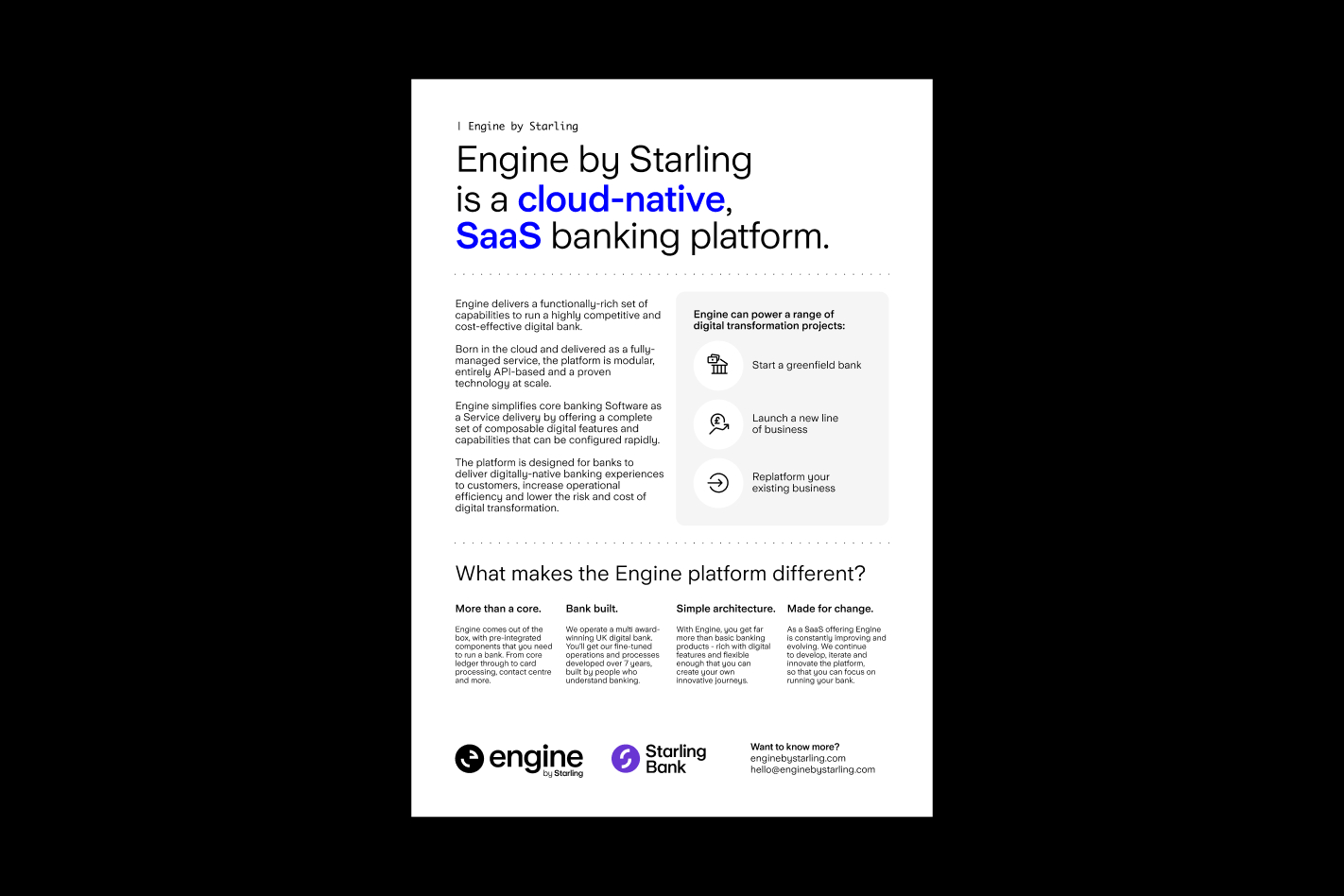

“We strongly believe Engine is the world’s most mature, cloud-native SaaS banking platform. It has been stress tested at scale for a number of years and solves some of the major challenges facing US financial institutions at the moment.”

Sam Everington, CEO, Engine

US financial institutions are under pressure to optimise their long-term costs. Deloitte’s MARGINPlus survey revealed that 50% of banks consulted cited ‘challenges with technology infrastructure’ as a key limiting factor. Engine offers a next-generation solution that solves a key challenge: unification.

Finding unity in a heavily fragmented market, across states and segments, is no mean feat. That degree of cohesion calls for configuration and agility, as banks and credit unions stay on top of a changing regulatory climate. Continued consolidation of financial institutions is also cautiously expected following a record number of credit union acquisitions of community banks in 2024.

By offering integration and migration capabilities which are designed to enable business transformation, Engine is well placed to support. This includes M&A, launching new business segments or creating a greenfield proposition, as well as enabling offerings which may well be revived under the new administration - who appear inclined to grant new bank charters nationwide.

“Engine can help unify your tech stack, unlock new growth opportunities and drive a cultural and operational shift in how your bank or credit union approaches innovation.”

Nick Drewett, Chief Commercial Officer, Engine

Unify customer segments

Our retail and business banking capabilities allow firms to fulfil the role of primary bank, twice. The disintermediation of retail and SME promotes continuity, engagement and loyalty amongst customers and members who are venturing beyond personal banking.

Post-pandemic hustler culture is here to stay; small businesses continue to multiply. The 33.2 million SME segment in the US is growing exponentially, with millions of new business applications submitted each year. Within these small businesses come sole proprietorships - 82% of SMBs - creating a unique opportunity to put a human face to business banking.

Engine’s self-service capabilities are designed to equip those working a 9 to 5 with the tools to manage their banking independently. Customers and members receive the same degree of service at 1am as they do at 1pm; this was a core Starling Bank principle which contributed to the acquisition of 9.4% of the UK SME market.

Launching a new business segment to promote continuity and expand your customer base is fully supported by Engine. In Q1 2025, AMP Bank launched its brand-new digital bank with Engine for small businesses in Australia - unlocking an underserved customer base in the region. Equipped with pre-integrated accounting solutions, saving spaces functionality and a seamless business onboarding experience, Engine’s solution allowed AMP to widen its footprint and deliver a customer-first proposition.

Unify the employee experience

‘A unified system helps avoid frustrating situations where customers must repeat themselves, and it ensures that updates—like transactions or account changes—are visible no matter which channel the customer uses.’ - RSM

An exceptional customer experience starts with an exceptional employee experience. Engine’s Management Portal is an end-to-end employee interface, encompassing holistic customer insights, a highly intuitive contact centre and transaction data feeds which are enriched by our in-house card processor. The platform removes the friction of manually reconciling information across multiple platforms, delivering a unified experience for onboarding agents, operations teams and fincrime specialists alike.

Accenture’s 2025 global banking study highlights the importance of cohesion across digital channels: ‘customers don’t see separate departments, they see one bank; banks should see themselves the same way’.

Engine’s front-to-back portal inherently delivers that unity, housing all operations in the bank in one place. Providing a holistic, 360° view, which removes the need for repetition and explanation, ensures customers feel known. Our clients can use AI tools after human interactions, such as automated wrap-up notes, to capture experiences with ease, and create a rich audit trail where trends and insights can be analysed and iterated upon. Technical capabilities have become so advanced that the homogenisation of the user experience is no longer a distant thought. It’s the human touch and personalisation that will allow firms to stand out.

Unification through reliability

Building trust with a customer base is essential. This starts with providing a robust, reliable digital channel which customers can depend on. Bank and credit union outages are a persistent pain point across the US: Capital One experienced a major outage earlier this year, following Bank of America’s October 2024 blackout which impacted 20,000 customers across their digital channels and ATMs. Navy Credit Union’s February outage affected an additional 2,000 members. Providing a resilient, fault-tolerant system which is built to expect failure rather than react to it has allowed Starling Bank - through Engine - to ensure that no reportable outage has occurred over eight years.

Our platform provides banks with a secure, resilient and scalable infrastructure, operating multiple live service instances in parallel so there is no single point of failure at any given time. At times of high load, during payday or concert ticket sales, Engine’s cloud-native infrastructure can be seamlessly expanded to withstand stress.

“Customers and members can rely on a bank built by Engine. This is a crucial element in becoming a consumer’s primary bank. Employees can rely on it, too - leveraging the 24/7 Service Desk and on-call technical support our managed service provides.”

Sam Everington, CEO, Engine

In spite of the growing popularity of digital channels, Tier 1s are investing in branches across the country to carve out local presences and compete with community banks. Bank of America is due to open 165 branches by 2026; J.P. Morgan’s investment stands at 500 branches by the following year. Branches seem to remain unaffected by wider industry modernisation. Founded on human-led interaction behind digital channels, Engine’s technology is well-equipped to support branch-based servicing capabilities - leveraging a culture of innovation to explore how the conventions of banking can be optimised. Combining tradition with outstanding technology generates a unique opportunity to rethink how these investments can be used to bring your customers and employees together.

Uniting standards to empower customers

Open banking is coming to the US.

After 15 years of socialising and defining a structure for open banking in America, Rule 1033 (the Personal Financial Data Rights Rule) is due for deployment until 2030, unlocking a $23 billion market.

Unity can only be achieved once customers and members have better control over their data. Open Banking offers an opportunity to deepen and enrich customer relationships, dismantling the perception that it leaves banks and credit unions exposed to their peers. US consumers have an average of five bank accounts, inundated with numerous apps and countless financial products. This behaviour is innate and unlikely to change overnight. Offering a best-in-class solution which unites disparate data sources seamlessly ensures that your bank or credit union becomes the ‘one-stop-shop’. PwC sees Open Banking as an opportunity to become a truly ‘customer-centric’ institution. This is ultimately achieved through successfully positioning your firm at the centre of the customer financial ecosystem.

Engine has a global alliance with Ozone API - who empower banks and financial institutions to adapt and thrive in the world of open banking. Ozone has been a member of the Financial Data Exchange (FDX) for nearly 5 years, elected as a Standards Setting Body by the Consumer Financial Protection Bureau (CFPB) earlier this year. Our partnership with Ozone enables our clients to remain compliant with Open Banking standards when they first hit the market and as they evolve.

Rule 1033 will go beyond creating a cohesive experience for retail and business banking customers. Customers will be drawn to a singular application: to make account-to-account payments, understand their personal finances and view account information and balances in one place. Whilst inherently ‘customer-centric’, achieving aggregation through Open Banking also provides a compelling addition to the value propositions of banks and credit unions across the US. Firms can deliver enhanced customer value by offering credit and pricing decisions tailored to the underlying applicant, or by offering bespoke products through a curated marketplace, strengthening their propositions and creating a truly unique, API-enabled experience.

1033 is a nascent concept for the US market. The novelty of Open Banking is what makes it most susceptible to change, as it naturally evolves into the Open Finance and Open Data space. Engine’s solution is built to grow, adapt and innovate so that clients can anticipate and respond to change in a cohesive and compliant way.

Conclusion

Engine offers banks and credit unions across North America the opportunity to strengthen their local presence through exceptional technology. Our cloud-native, innovative SaaS banking solution allows firms to defend against new entrants or become the new entrant that incumbents fear. In a market rife with competition, proactivity is essential. Banks evaluate core transformation every 5-10 years yet act on replacing it every 20, waiting for "end-of-life" results in years of stunted growth in the interim.

Benefit from a lower cost to serve, increased customer advocacy and a best-in-class, universal experience. Change can start today.

Contact us

Want to know more?

Whether you’re launching a new digital bank or migrating from a legacy platform: let’s discuss how Engine can help. Share details about your requirements and we will be in touch.

Are you looking for a BaaS solution in the UK?

Speak to Starling’s dedicated B2B team to find out more about the services provided.